※ This article is for informational purposes and personal analysis only—not investment, legal, tax, or immigration advice, and not a recommendation to buy or sell any property or financial product. Verify figures, rules, and market data against official sources and consult qualified professionals; you are solely responsible for your decisions. Information reflects the time of writing and may change afterward.

The global asset market is facing a massive financial barrier, exhibiting a distinct mix of trends. Korea aggressively implemented Stage 2 Stress DSR — Debt Service Ratio, which limits borrowing capacity based on income and potential rate hikes — on September 1, 2024 [Source: Financial Services Commission, press release ‘Stage 2 Stress DSR Implementation from September 1’, 2024-08-20] to curb household debt. Meanwhile, Japan ended its historic negative interest rate policy and raised its policy rate to around 0.25% on July 31, 2024 [Source: Bank of Japan, public statement ‘Decisions on the Monetary Policy Meeting’, 2024-07-31], pivoting to a tighter monetary stance.

What strikes me as critical here is that despite credit tightening and interest rate hikes, a highly precise line is being drawn in the sand of asset market polarization. The old formula, where entire regions rose in unison, is completely broken. In the end, we must identify the intrinsic scarcity that remains undamaged by adversity. I believe this sharp eye will be the defining key to survival in the unfolding asset market.

MACRO BARRIER

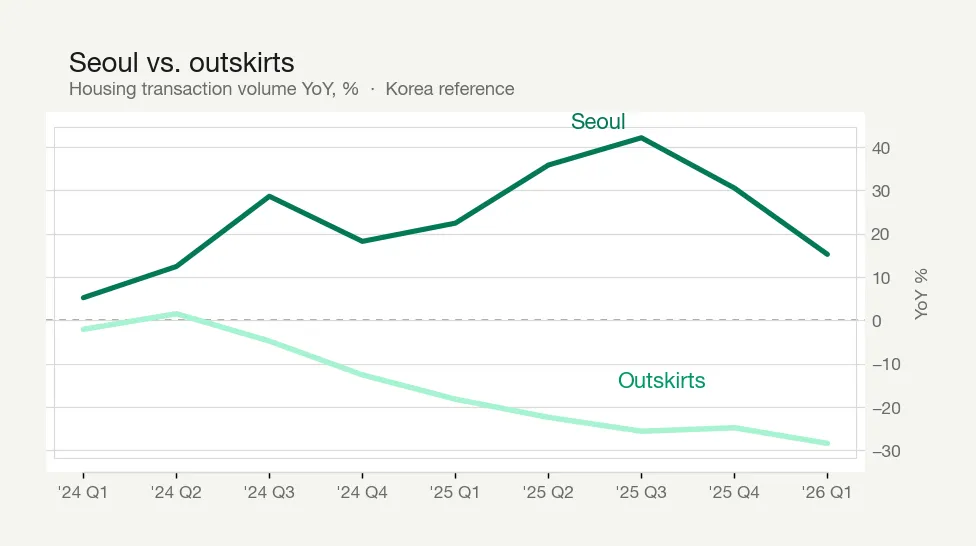

• Korea: Stage 2 Stress DSR (implemented Sept 1, 2024) ➔ Outskirt transaction volume plummets by 24.4% (MoM)

• Japan: BOJ rate hike (0.25% on July 31, 2024) ➔ Pre-owned mansions rise +2.2% MoM (23 wards surge +3.9% to record high) (as of Sept 2024)

ULTRA SCARCITY

• Seoul: Banpo/Seocho standard apartments Raemian One Bailey exceed 5 billion KRW without loans (Aug 2, 2024 record high)

• Tokyo: Minato/Shibuya landmark mansions maintain strong downside resilience & upward trends (as of Sept 2024)

1. Fact Check: How Capital Navigates Around Regulation and Rate Barriers

Recently, the Korean real estate market has revealed a league of affluent investors who are completely insulated from credit restrictions. As strict loan regulations apply across the metropolitan area, housing transaction volumes in outlying regions (Gyeonggi and Incheon) for September 2024 plummeted by 24.4% compared to the previous month [Source: Ministry of Land, Infrastructure and Transport, press release ‘September 2024 Housing Statistics Announcement’, 2024-10-31], reflecting a rapid slowdown.

On the other hand, the flagship complexes in Banpo-dong, Seocho-gu, tell a completely different story. As of August 2024, standard 84㎡ apartments (such as Raemian One Bailey) crossed the 5 billion KRW threshold, funded entirely by equity without a single loan [Source: Ministry of Land, Infrastructure and Transport, Real Estate Transaction Disclosure System, transaction date 2024-08-02]. New records approaching 150 million KRW per pyeong — a Korean unit of area, roughly 3.3 square meters — are consistently being set. It is a striking anomaly: credit restrictions act as a protective barrier for the high-end market, compacting capital into prime locations where leverage is irrelevant.

This polarization is observed with a strong sense of déjà vu across the sea in Tokyo. As floating mortgage rates began to react to the Bank of Japan’s — BOJ, the central bank of Japan — gradual rate hikes, Tokyo’s pre-owned mansion market maintained its strong stance within the post-pandemic uptrend, rising by 2.2% month-on-month as of September 2024 (with average prices in the central 23 wards jumping 3.9% MoM to 80.53 million JPY, surpassing the 80 million JPY threshold for the first time in history) [Source: Tokyo Kantei, report ‘Tokyo Metropolitan Area Pre-owned Mansion 70㎡ Price Trends’, 2024-10-24]. However, weighed down by slowing demand in outlying suburbs and escalating interest rate pressures, chase-buying by broader end-users has grown increasingly cautious.

Yet, landmark mansions in ultra-core downtown areas (the central 3 wards) like Minato, Shibuya, and Nihonbashi maintain ironclad downside resilience [Source: Real Estate Economic Institute, report ‘Metropolitan Area Mansion Market Trends (September 2024)’, 2024-10-17]. Capital from global investors lured by the weak yen continues to flow steadily into these prime assets. Combined with the cost-push effect of skyrocketing materials and labor costs, new high-end downtown developments are proving their robust defensive strength, laughing off the headwind of rising interest rates.

2-1) The Counter-Hypothesis and Its Limits (Bear Case)

The fundamental premise of downside resilience for ultra-scarce assets could also crack under specific macroeconomic stress scenarios. If the global macroeconomy moves beyond a prolonged period of high interest rates (Higher for Longer) into a systemic default crisis or severe stagflation, causing a credit crunch that freezes the cash flows of both domestic and international investors, high-end real estate will also find it difficult to avoid a steep liquidity discount.

However, even under such an extreme Bear Case scenario, the relative value of ultra-scarce assets is preserved. When asset prices across the entire market face downward pressure, outlying assets heavily reliant on financial leverage may plummet below their liquidation value. In contrast, ultra-scarce assets backed by strong intrinsic costs and cash reserves will undergo a relatively mild decline and demonstrate the quickest rebound once the economy recovers. In other words, while they cannot completely avoid absolute declines, their marginal advantages—relative superiority and long-term recovery resilience—will remain intact.

2. Interpreting the Anomaly: The Capital Dust Collector Effect

These two contradictory phenomena offer us profound insights. Credit regulations and BOJ rate hikes are undoubtedly macroeconomic headwinds that dry up market liquidity. However, when the broader market’s financial pipeline narrows, capital does not disperse evenly. Paradoxically, it concentrates into a tiny fraction of the most secure, irreplaceable safe-haven assets.

[IMPORTANT] Capital Dust Collector Effect: As strong pressure like liquidity contraction is applied, capital adheres even more tightly to the top 1% ultra-scarce assets. The macro adversity paradoxically acts as a shield to defend the safe-haven status of prime locations.

At this juncture, I believe we must dismantle the broad myth of invincibility—the blind assumption that “it’s safe just because it’s Gangnam” or “it’s central Tokyo.” During asset stagnation, extreme differentiation occurs even within Gangnam or Tokyo’s 23 wards. Price trends diverge sharply based on micro-location, complex scale, and the sheer scarcity of infrastructure.

From a practical standpoint, it goes beyond simply choosing a good neighborhood. We must slice the seemingly scarce high-end market even finer. The critical task today is to cultivate a precise eye to filter out the “scarcity within scarcity” — assets that are physically impossible to replicate.

3. Investor Action: Summary and Checklist

- Evaluate Credit Immunity: Analyze whether the asset’s price is highly vulnerable to credit caps and floating rate hikes, or if it is a prime asset capable of defending its downside purely through intrinsic replacement costs (material/labor) and all-cash purchasing power.

- Dismantle Prime Location Biases: Never rest easy just because of the “Gangnam” or “Central Tokyo” label. Update your monthly individual assessments to verify whether the physical scarcity of the landmark location remains uncompromised.

- Align with Global Capital Flows: Monitor the specifications of assets chosen as “Wealth Parking Zones” by international high-net-worth individuals during tightening cycles. Watch foreign exchange (FX) flows and rebalance your portfolio accordingly.

4. Conclusion: Sharpening Your Selective Lens

The double barrier of credit regulations and interest rate hikes is a rigorous test of the asset market’s resilience. It will inevitably separate the counterfeit from the genuine. In this volatile period, blindly believing in unconditional price appreciation is reckless. Only deep scarcity, combined with irreplaceable location and replacement cost defense, is likely to hold its ground.

Ultimately, the winners of the upcoming real estate market will not be determined by the sheer volume of their capital. Victory will belong to those with the “selective lens” to precisely filter out truly scarce assets. At this stage, instead of chasing purchases in a rush, the best strategy is to quietly sharpen this selective vision.

![Where to Live in Tokyo [Ep.12] Has Tama New Town Really Failed? Machida, Tama City & Inagi [2026]](https://gsfark.com/assets/images/blog/tokyo-machida-tama-inagi-hero-og.jpg)

![Where to Live in Tokyo — The 23 Wards Guide [Ep.11] The Real Housing Prices of Western Tama Hidden Behind Averages: Hachioji, Hino, and Akishima](https://gsfark.com/assets/images/blog/tokyo-hachioji-hino-akishima-hero-og.jpg)