![Korea–Japan Inheritance Tax: Residency and Japan’s 10-Year Test [2026]](https://gsfark.com/assets/images/blog/korea-japan-inheritance-gift-tax-cross-border-basics-hero-og.jpg)

※ This article is for informational purposes and personal analysis only—not investment, legal, tax, or immigration advice, and not a recommendation to buy or sell any property or financial product. Verify figures, rules, and market data against official sources and consult qualified professionals; you are solely responsible for your decisions. Information reflects the time of writing and may change afterward.

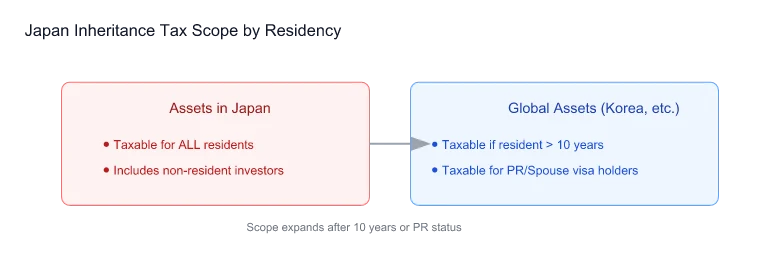

Living in Japan for ten years does not automatically make every worldwide asset subject to Japanese inheritance or gift tax. The scope can depend on both parties’ address, nationality, residence status and prior residence, as well as the location of each asset.1

The 10-year threshold is therefore not the answer. It is the point at which the classification table should be opened.

1. Does ten years in Japan automatically trigger worldwide taxation?

No. For these rules, a Japanese “temporary resident” generally means a person who holds a qualifying residence status at the relevant time and had an address in Japan for no more than ten years in total during the previous 15 years.23

That definition does not guarantee Japan-only taxation. For an inheritance, the classification of the heir and the decedent must be read together. For a gift, the recipient and donor must be considered together.

Worldwide scope may apply when the recipient or heir falls within an unlimited-taxpayer category. The result can also turn on nationality, residence status, prior Japanese residence and asset location—not a single stopwatch.

| Check first | Question |

|---|---|

| Recipient or heir | What are their address, nationality and residence status? |

| Donor or decedent | What are their address, nationality and Japanese residence history? |

| Time | How many years of Japanese address fall within the relevant lookback? |

| Asset | Where is each property, account or security located for tax purposes? |

This is why “foreign national plus under ten years equals limited taxpayer” is unsafe as a general rule.

2. When does Japan’s seven-year gift addback actually apply?

It did not switch immediately to seven years in 2024. For inheritances beginning on or before December 31, 2026, the previous three-year period applies.14

For inheritances beginning from January 1, 2027 through December 31, 2030, the period runs from January 1, 2024 to the date of death. The full seven-year lookback applies to inheritances beginning on or after January 1, 2031.

The gift date and the date the inheritance begins must therefore be tested together.

3. Is Korea’s recipient-based inheritance tax set for 2028?

Not as enacted law. The Korean government published a legislative proposal to move from taxing the estate as a whole to taxing the property acquired by each heir.7

Around 2028 has been described as a target subject to legislation and implementation work. Parliamentary review and later legislation can change both the content and timing.

A separate proposal to cut the top rate was not part of this recipient-based reform plan. It should not be presented as a scheduled 2028 change.

4. Does the Korea–Japan tax treaty remove inheritance-tax overlap?

Korea and Japan do not have a separate bilateral inheritance and gift tax treaty. The bilateral income tax treaty does not automatically settle inheritance or gift tax overlap.6

Domestic foreign-tax-credit rules may reduce double taxation. Korea’s implementing rule, for example, provides a calculation and ceiling for crediting foreign inheritance tax.5

Residual tax can remain because credit limits, valuation methods and filing dates differ. Tax paid in one country does not by itself prove that the liability in the other country is zero.

5. What is the practical order of checks?

- Classify the heir and decedent, or the recipient and donor, separately.

- Map the tax location of each property, account and security.

- Identify filing duties in Korea and Japan.

- Calculate each country’s tax under its own rules.

- Test the available foreign tax credits and any residual liability.

This is a fact-finding sequence, not a tax-saving formula. Before filing, provide the same residence timeline and asset list to qualified Korean and Japanese tax professionals so the two calculations can be reconciled.

The useful first question is not simply, “Has ten years passed?” It is: How is each person classified, and where is each asset located?

Recommended Series

- Corporate vs Personal Ownership: Tax Comparison

- Japan Visa Routes: PR and Business Manager Fast-Tracks

- Tokyo Office Market 2026: Vacancy and Rent Trends

This article provides general information. The applicable scope and tax amount depend on the facts and the law in force at the relevant time.

![New vs. Pre-Owned Mansions in Japan — Prices, Depreciation & Repair Costs [2026]](https://gsfark.com/assets/images/blog/japan-shinchiku-vs-chuko-mansion-investor-guide-hero-og.jpg)