※ This article is for informational purposes and personal analysis only—not investment, legal, tax, or immigration advice, and not a recommendation to buy or sell any property or financial product. Verify figures, rules, and market data against official sources and consult qualified professionals; you are solely responsible for your decisions. Information reflects the time of writing and may change afterward.

The internet is flooded with rosy success stories about earning passive income from Japanese real estate. However, at GSF, we have encountered many investors who have suffered significant financial losses due to poor structuring and insufficient due diligence.

Today, I examine a case study of a failed investment to highlight three critical risks hidden beneath the surface of the Japanese market. I hope this record serves as a shield for your hard-earned capital.

1. The Betrayal of Subleasing: Who is the ‘assured Return’ Really For?

Novice investors are often drawn to the phrase ‘assured Rent.’ Japanese management companies offer ‘sublease’ contracts where they take on the vacancy risk in exchange for a margin of the profit.

- Failure Case: Investor ‘A’ purchased a new-build condo with a 10-year rent guarantee. Two years later, the management company demanded a rent reduction citing “market changes,” threatening to cancel the contract if the investor did not comply.

- Lesson: Japan’s Act on Land and Building Leases strongly protects tenants—which in this case is the management company. Even if the contract says ‘fixed,’ the company has a legal right to request a reduction. Conversely, the owner often needs ‘justifiable grounds’ or must pay a heavy penalty to terminate the lease. A sublease is often a tool to protect the management company’s profits, not yours.2

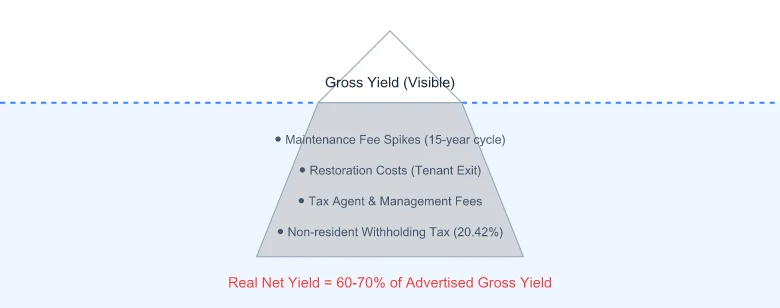

2. The Ambush of Hidden Costs: The Tip of the Iceberg

Investment yield is not simply a calculation of the purchase price and the monthly rent.

- Failure Case: Investor ‘B’ bought a second-hand condo with a 6% gross yield. Shortly after the purchase, the building management association decided on a ‘Large-Scale Repair,’ tripling the monthly maintenance contribution. After paying for restoration costs when the tenant moved out, the annual yield turned negative.

- Lesson: Japanese real estate is an ‘aging asset.’ You must review the ‘Important Matters Explanation’ (Juyo Jiko Setsumei) to check the repair plan and the accumulated reserve fund balance. Real net yield is typically 1.5% to 2% lower than the gross number.

3. The Blade of Tax Audits: Borders Are Not a Shield

Thinking “the Japanese tax office won’t know about my overseas assets” is a dangerous arrogance.

- Failure Case: Investor ‘C’ reported rental income only in their home country and neglected to file in Japan. A few years later, the National Tax Agency (NTA) cross-referenced bank remittance records with the real estate registry. ‘C’ was hit with massive back taxes, penalties, and interest.

- Lesson: Japan participates in the Common Reporting Standard (CRS), exchanging financial information with other countries. Even as a non-resident, you must appoint a Tax Agent (Nozei Kanrinin) and file in Japan. Tax evasion is not a ‘strategy’; it is a crime that can destroy your entire investment.1

4. Conclusion: Learn Not to Lose First

In the world of investment, ‘not losing’ is more important than ‘how much you make.’ The Japanese market is stable, but its rules are strict and conservative.

- Trust documents over a broker’s words.

- Factor tax and legal fees into your ‘initial capital’ calculation.

- Ensure you have the financial stamina to survive the worst-case scenario (vacancy + rate hike + repairs).

At GSF, we listen to potential failure stories as closely as we do success stories. Removing the thorns behind the flashy yields is the start of what we call ‘Warm but Rational Investing.’

Data freshness (April 2026): BOJ policy rate 0.75 %, 10-year JGB ≈ 2.43 %, TSE REIT Index ≈ 1,916, Tokyo 5-ward vacancy 2.22 % (Miki Shoji Q1 2026), Q1 2026 inbound tourists 10.68 M (JNTO). Verify the latest from linked sources before acting.

Investor Action: Session Summary & Check

- Review: Re-examine past investment losses caused by ‘negligent management’ or ‘information asymmetry’.

- System: Digitize your buy-hold-sell checklists instead of relying on gut feeling.

- Mindset: Set a maximum drawdown limit in advance and establish mechanical trading rules to avoid emotional decisions.

Recommended Series

- Korea-Japan Inheritance Tax: The 10-Year Rule Trap

- Managing FX Risks: Principles for the Weak Yen Era

- Corporate vs Personal Ownership: Decision Guide

![Korea–Japan Inheritance Tax: Residency and Japan’s 10-Year Test [2026]](https://gsfark.com/assets/images/blog/korea-japan-inheritance-gift-tax-cross-border-basics-hero-og.jpg)

![New vs. Pre-Owned Mansions in Japan — Prices, Depreciation & Repair Costs [2026]](https://gsfark.com/assets/images/blog/japan-shinchiku-vs-chuko-mansion-investor-guide-hero-og.jpg)