※ This article is for informational purposes and personal analysis only—not investment, legal, tax, or immigration advice, and not a recommendation to buy or sell any property or financial product. Verify figures, rules, and market data against official sources and consult qualified professionals; you are solely responsible for your decisions. Information reflects the time of writing and may change afterward.

In Japan, real estate investment is a “Tax Game.” Even if you secure a property with a high gross yield, a poor ownership structure can lead to an effective tax rate of over 50%, wiping out your cash flow.

For foreign investors and non-residents, the choice between Personal Ownership and Corporate (GK/KK) Ownership depends on your long-term exit plan and the scale of your portfolio. Today, we break down the pros and cons of each structure based on the latest 2026 tax standards.

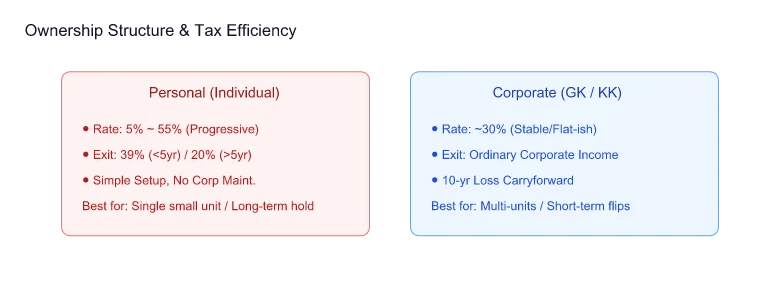

1. Personal Ownership: Simple but Punitive for High Earners

Personal ownership is easy to set up but subject to Japan’s steep Progressive Tax Rates.

- Income Tax (Rental Income): Combined with other Japan-sourced income, rates range from 5% to 45% (plus a 10% inhabitant tax for residents, totaling 55%).1

- Capital Gains Tax (The 5-Year Rule): This is the most critical factor for personal owners.

- Short-term (Held < 5 years): Approx. 39% tax on gains (30.63% for non-residents).

- Long-term (Held > 5 years): Approx. 20% tax on gains (15.315% for non-residents).

- Note: For non-residents, the inhabitant tax portion may differ, but the federal 30% / 15% split remains the benchmark.

- Withholding Tax: Non-residents are subject to a 20.42% withholding tax on gross rent if the tenant is a corporation or uses the property for business.4 This is a cash flow burden, though it can be reconciled via a tax return.

2. Corporate Ownership: Predictable Rates and Diverse Deductions

Setting up a Japanese company (Godō Kaisha or Kabushiki Kaisha) offers a more stable tax environment for serious investors.

- Effective Tax Rate: For small to medium-sized corporations, the effective tax rate (including enterprise and inhabitant taxes) is generally capped around 30% to 34%.3

- Loss Carryforward: Corporations can carry forward tax losses for up to 10 years, which is vital for offsetting initial acquisition costs and depreciation.

- Expense Flexibility: A wider range of expenses, including travel for property inspections, management fees, and even salaries for family members (under certain conditions), can be deducted.

- No “5-Year Rule”: Corporations do not have a separate “long-term” vs “short-term” capital gains rate. All gains are treated as ordinary corporate income and taxed at the effective rate, providing more flexibility for timing your exit.

3. Visual Comparison: Tax Liability Mapping

4. Which One Should You Choose?

The “Break-even Point” for switching to a corporate structure usually occurs when your taxable rental income exceeds 9 million JPY to 15 million JPY (approx. 9M JPY in net taxable rental income) per year, or when you plan to build a portfolio of 3+ units.

Choose Personal If:

- You are buying a single small apartment for a long-term hold (10+ years).

- The annual rental profit is low, keeping you in the lower progressive brackets (below 20-30%).

- You want to avoid the annual corporate maintenance costs (approx. 70,000 JPY minimum tax + accounting fees).2

Choose Corporate If:

- You plan to sell within 5 years (avoiding the 39% individual short-term tax).

- You are an active investor looking to leverage bank financing (Japanese banks prefer lending to local entities).

- You want to manage your inheritance tax by distributing shares or setting up a family office.

5. Conclusion: Strategy Before Signature

Changing ownership after the purchase is expensive (re-paying registration taxes and real estate acquisition taxes). At GSF, we always advise clients to finalize the tax structure before signing the sales contract.

Investing in Japan is not just about the property; it’s about the “Vessel” you use to hold it. Make sure your vessel is built for the long haul.

Data freshness (April 2026): BOJ policy rate 0.75 %, 10-year JGB ≈ 2.43 %, TSE REIT Index ≈ 1,916, Tokyo 5-ward vacancy 2.22 % (Miki Shoji Q1 2026), Q1 2026 inbound tourists 10.68 M (JNTO). Verify the latest from linked sources before acting.

Investor Action: Session Summary & Check

- Entity: If annual rental income exceeds 20M JPY, consult a tax accountant about the tax benefits of switching to a corporate entity.

- Expenses: Optimize yield by listing deductible corporate expenses like labor, travel, and management fees in advance.

- Succession: If planning to pass on assets to children, develop a long-term plan to see if gifting corporate shares is better than personal asset gifts.

Recommended Series

- Korea-Japan Inheritance Tax: The 10-Year Rule Pitfall

- Japan Visa Paths: Business Manager & Highly Skilled Professionals

- Tokyo Office Vacancy 2026: Supply and Demand Shifts