※ This article is for informational purposes only and is not investment, legal, tax, or immigration advice. Figures, rules, hours, and operational details were accurate when published—verify with official sources before you rely on them.

Talking about ‘warmth’ at the heart of capitalism can sometimes seem naive or inefficient. There is no room for emotion in the cells of an Excel sheet, as yields and exchange rates are driven solely by cold logic.

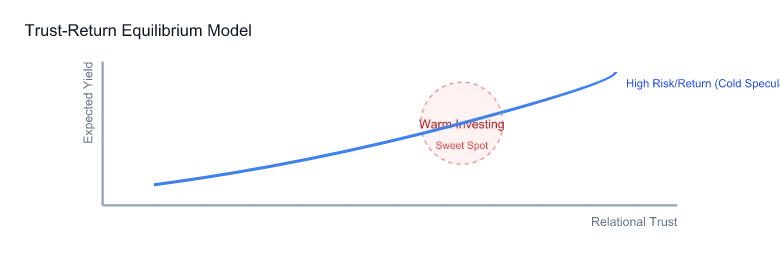

However, after observing the success and failure of numerous investments, the conclusion is clear: what protects the coldest numbers is ultimately the warmest quality of relationships. GSF defines ‘Warm Investing’ not as vague goodwill, but as a highly engineered strategic framework designed to minimize ‘coordination failure risks’ and maximize resilience during crises.

1. The ‘Relational Value-Add’ That Excel Misses

Investment models compress reality into variables like interest rates, vacancy, and FX. But when markets shake and unexpected variables explode, it is ‘people,’ not models, who control those variables.

- Responsiveness in Crisis: How responsibly a contractor moves when a building issue arises, or what win-win solution a landlord offers when a tenant is in trouble. These ‘unstructured data’ points ultimately determine the long-term value of an asset.

- Cultural Context: Especially in cross-border investments like those between Korea and Japan, where business cultures differ, trust beyond language significantly lowers transaction costs.

2. The 3 Pillars of the Warm Investing Risk Scorecard

GSF always places a ‘Trust Equilibrium’ alongside expected yields. The indicators of ‘warmth’ we measure are as follows:

- Transparency: Is information symmetric, and are signs of failure shared honestly?

- Sustainability: Is the structure designed to last for generations without exhausting relationships for short-term gain?

- Execution: Is there the ‘grit’ to follow through on promises to the very end?

3. Practical Application: ‘Diligence’ the People First

Before deciding on an investment, GSF conducts ‘Reputation and Philosophy Due Diligence’ on partners even before looking at the numbers.

- Scenario-Based Questioning: I ask, “If the exchange rate spikes by 20%, what choice will you make?” I read their priorities in the thought process leading to the answer, rather than just the answer itself.

- On-Site Inspection: I sense the ‘temperature’ of asset management through the eyes of the manager, the expressions of the residents, and the minor maintenance details of the building.

- The Principle of Minimum Weight: High-yield assets lacking assured trust never exceed 5% of my portfolio.

4. Conclusion: “Analyze Coldly, Own Warmly”

‘Warm Investing’ is not a symbol of weakness. Rather, it is the ‘toughest attitude of an investor’ who survives all market noise to eventually secure returns. While numbers don’t lie, it is the human heart that ultimately moves those numbers.

GSF will continue to integrate human warmth into cold data analysis. I believe this is the surest way to protect and grow assets in an era of extreme volatility.

5. When Cold Models Fail: Three Cross-Border Case Studies

Abstract principles become concrete when stress-tested against real market dislocations. Below are three composite scenarios—drawn from recurring patterns GSF observes in the Korea-Japan investment corridor—that illustrate where purely quantitative approaches consistently underperform.

Case A: The Contractor Who Did Not Pick Up the Phone

An investor purchased a mid-size apartment building in Edogawa-ku with an IRR projection of 12.3% based on prevailing cap rates and occupancy data. Within eight months of closing, a water pipe failure in one of the upper units caused damage to three floors. The property management company—selected solely because their fee was 0.3% below the next bidder—took 11 days to mobilize a certified repair contractor and communicated only via automated email.

The financial cost of the repair was modest. The reputational cost was not: two long-term tenants gave notice within 60 days, citing the response time as the deciding factor. Vacancy dragged actual IRR to 6.8% in year one. A warm-network property manager who had been passed over because of fees would have had a repair crew on-site within 24 hours—standard expectation within professional referral networks.

Case B: The Partner Who Moved Goalposts After FX Shifted

A Korean LP committed capital to a co-investment structure where a Japanese GP held the local operating entity. When the yen depreciated sharply in 2022–2023, the GP unilaterally restructured the fee calculation to minimize yen-denominated distributions—a move that was technically permitted under a loose clause in the operating agreement but was never discussed during deal negotiation.

The LP had no legal recourse because the clause existed. The LP did have a choice about future deals—and made it. The GP lost access to Korean LP capital networks that had taken years to build. No spreadsheet model had assigned probability to this outcome because it required modeling the GP’s ethics under financial pressure, not just their historical returns.

Case C: The Tenant Whose Word Was Enough

In contrast: a residential owner in Shinjuku with a Korean tenant had a vacancy threat when the tenant lost their corporate housing allowance mid-lease. Rather than initiating immediate eviction proceedings, the owner negotiated a three-month rent reduction with full arrears recovery structured over the following year. The tenant stayed for an additional four years, referred two colleagues as tenants for adjacent units, and became an informal community liaison who kept vacancy near zero across the portfolio.

The reduced rent cost the owner roughly ¥480,000 over three months.1 The avoided vacancy cost and referral value were approximately ¥2.4 million over four years. Warm calculation, cold outcome.

6. Building Trust Capital: A Practical Framework for Cross-Border Investors

Trust is not a soft variable—it is a capital asset with real yield. For Korea-Japan cross-border investors specifically, trust capital operates on three levels that require active construction.

Level 1 — Language and Cultural Fluency This is entry-level. It does not mean you must be bilingual, but it does mean investing in a local partner or advisor who operates with genuine bilingual capacity and understands the unspoken norms of Japanese business conduct: the weight placed on nemawashi (prior consultation), the meaning of silence in a negotiation, and the distinction between tatemae (official position) and honne (actual intent). Misreading these costs money.

Level 2 — Network Reciprocity Korean investors with sustained presence in Japan build relationships not transactionally but through reciprocity over time. This means sharing deal flow information before requiring it, introducing Japanese counterparts to Korean networks without extracting a fee, and showing up consistently to industry events in both Seoul and Tokyo even when no immediate deal is in view. The Japanese business culture places significant weight on continuity of relationship; dropping in only when there is a transaction to execute reads as opportunism.

Level 3 — Structural Transparency At the most sophisticated level, warm investing means designing deal structures that do not exploit information asymmetry. This includes proactively sharing valuation methodology with co-investors, flagging downside scenarios before capital is committed, and building clawback provisions into GP compensation structures that align incentives across the full holding period. In an era where Korean investors are increasingly scrutinizing Japanese GPs for governance quality, the GP who volunteers this transparency before being asked commands a measurable premium in LP trust—and access.

The Compounding Effect: Trust capital compounds non-linearly. A single high-quality referral from a trusted network node can unlock LP relationships, regulatory introductions, or off-market deal flow that no amount of cold outreach replicates. This is not idealism—it is the structural advantage of patient, warm capital in a market where most international flows remain opportunistic.

Philosophical Reflections

- Which asset in your portfolio has the highest ‘people risk’?

- Do you have enough ‘Trust Capital’ to resolve a dispute through dialogue before resorting to legal action?

- How is your investment adding ‘warmth’ to the world? (Value beyond ESG)

Recommended Essays

- Post-Mortem of a Failure: 3 Lessons

- Seoul and Tokyo: Reading Two Markets as One

- FX Volatility and Investment Principles

Investor Action: Session Summary & Check

- Essence: Ask yourself if you are investing in spaces that improve ‘human quality of life’ rather than just chasing price growth.

- Sustainability: Verify if the location has the community and infrastructure to be loved 10 years from now, beyond short-term trends.

- Empathy: Create ‘sticky assets’ by providing values tenants truly desire—safety, comfort, and dignity.

![Buying a Condo in Japan: 10 Things to Check Before You Sign [2026]](https://gsfark.com/assets/images/blog/buying-property-japan-checklist-before-you-commit-hero-og.jpg)